So you want to start a title company. Before you get tangled in the weeds of legal structures and underwriting agreements, you have to get the lay of the land. It’s a detailed world, one that lives at the intersection of real estate law and sharp business operations. Getting it right from day one is everything. This guide provides a clear roadmap, highlighting how modern tools can give your new venture an immediate competitive advantage.

Navigating the Modern Title Industry

Before we jump into the nuts and bolts, let's zoom out. The title industry is the bedrock of the real estate market. It provides that critical peace of mind, assuring everyone involved that a property’s ownership is clean and clear. This whole business is built on precision, trust, and knowing the regulations inside and out.

Knowing how to start a title company isn't just about following a checklist. It's about spotting opportunities, figuring out what clients really need, and positioning your new agency to go head-to-head with the old guard. Your initial market analysis will drive every decision you make, from your business plan to how you get your first customer.

Before we dive deeper, here’s a quick look at the core components you’ll be assembling.

Core Pillars for Launching Your Title Company

This table breaks down the essential components required to establish a compliant and competitive title company from the ground up.

| Pillar | What It Involves | Why It's Non-Negotiable |

|---|---|---|

| Legal & Licensing | Choosing a business structure (LLC, Corp), getting state licenses, and securing bonds. | This is your ticket to operate legally. Skipping a step here can shut you down before you even start. |

| Underwriter Partnership | Vetting and selecting a national underwriter to back your policies. | Without an underwriter, you can't issue title insurance. They provide the financial security your policies need. |

| Tech Stack | Implementing modern software for title production, escrow, and client communication. | This is your competitive edge. Smart technology like TitleTrackr delivers speed, accuracy, and a superior client experience. |

| Operational Workflow | Defining your step-by-step processes for handling a file from open to close. | A smooth workflow prevents errors, keeps clients happy, and lets your team operate at peak efficiency. |

Think of these as the foundation. Get them right, and you're building on solid ground.

Understanding the Market Opportunity

The title industry is surprisingly resilient. It often holds steady even when the rest of the real estate market gets a little shaky. This stability creates a great runway for new companies.

Case in point: the U.S. title insurance sector recently pulled in around $4.5 billion in premiums in a single quarter. The demand is clearly there. If you want to dig into the numbers, you can explore a full report on recent title insurance performance.

But there’s a catch. The market is concentrated. A handful of huge underwriters, like First American Title Insurance Co., have a massive footprint.

For a new agency, this means you aren't just competing with other local firms; you're operating within an ecosystem shaped by these industry giants. Understanding their role is crucial for selecting the right underwriting partner and carving out your niche.

Your job is to figure out what you can offer that they can't. Maybe it’s unmatched local expertise, ridiculously good customer service, or hyper-efficient closings thanks to smart technology. That’s how you win.

The Role of Technology in Gaining a Competitive Edge

Here’s where being the new kid on the block is a massive advantage. You can build your entire operation around modern tech from the very beginning.

Many established firms are stuck with clunky, outdated systems and manual processes that are slow and invite mistakes. By adopting an integrated platform right away, you can deliver a closing experience that’s faster, more transparent, and far more reliable.

This is exactly where a system like TitleTrackr comes in. Instead of trying to patch together different tools for title production, document management, and client updates, a unified platform puts it all in one place. Suddenly, a small, nimble team can punch way above its weight.

A tech-first approach gives you some serious benefits:

- Reduced Manual Entry: Automation slashes the risk of human error in critical documents and financial figures.

- Improved Client Communication: A central portal gives agents, lenders, and buyers real-time updates on their transaction. No more "just checking in" calls.

- Faster Turnaround Times: Smooth, automated workflows speed up the entire closing, from opening the file to issuing the final policy.

- Enhanced Compliance: Good software has compliance built-in, helping you make sure all state and federal rules are met and documented perfectly.

Using technology strategically isn't a "nice-to-have" anymore. It's how you immediately stand out in a crowded field. You won’t compete on size or legacy—you’ll compete on speed, accuracy, and a client experience that makes people want to work with you again.

Once you’ve got a solid read on the market, it’s time to get down to brass tacks: building the legal and financial framework for your business. This isn't about high-level strategy anymore. It’s about careful, meticulous execution.

Getting these foundational pieces right from day one is non-negotiable. This is the stuff that dictates your agency’s ability to operate legally, protect you from liability, and—most importantly—handle client funds with integrity. Think of it as the structural steel of your new company.

Choosing Your Business Structure

The first real step is deciding on a legal entity for your agency. This single choice will impact everything from your personal liability to how you file your taxes. You should absolutely talk to an attorney and a CPA, but it's good to walk into that conversation knowing the lay of the land.

For most new title agencies, the choice usually boils down to two popular structures:

- Limited Liability Company (LLC): This is a really flexible option that shields your personal assets from business debts and lawsuits. It’s pretty simple to set up and maintain, striking a great balance between protection and ease of use.

- S Corporation (S-Corp): An S-Corp can unlock some nice tax advantages. It lets you pay yourself a salary and take dividends, which can potentially lower your self-employment tax bill. The trade-off is that it comes with more formal requirements, like holding board meetings and keeping very detailed records.

So, which one is for you? An LLC is often the go-to for its simplicity when you're just starting out. As your business grows and profits climb, an S-Corp might start to make more financial sense.

Securing State Licensing and Bonds

With your business entity registered, the next hurdle is getting licensed by the state. Every state has a department of insurance or a similar regulatory body that oversees title agencies. Their websites are your best friend here, but the process generally involves the same core pieces.

You'll typically need to show proof of your business registration, pass a background check, and in many states, pass a licensing exam. Don’t underestimate that test. It covers insurance principles, title law, and real estate procedures. Some states even require pre-licensing courses to get you ready.

Beyond the license itself, you'll need to get bonded. These aren't optional—they’re a mandatory safeguard for consumers.

Surety Bond: This is a guarantee that your company will live up to its legal and contractual promises. If you don't, the bond gives your clients financial recourse.

Fidelity Bond: This one protects against losses from employee dishonesty or fraud, like someone dipping into escrow funds. It’s a crucial layer of internal protection.

Bond amounts vary quite a bit by state but often start around $50,000 or more. Securing them sends a clear message to clients and underwriters that your agency is financially sound and operates with integrity.

Navigating Essential Insurance Coverage

While bonds protect your clients, insurance is what protects your business. The absolute most critical policy you’ll buy is Errors & Omissions (E&O) insurance. This is your professional liability coverage.

Imagine a simple clerical error in a legal description slips through the cracks, only to surface years later as a massive claim against the property’s title. E&O insurance is what covers your legal defense and any potential damages from that kind of mistake. Most states require a minimum coverage of $250,000, but don’t be surprised when underwriters demand policies of $1 million or more. This is not the place to pinch pennies.

Managing Compliant Escrow Accounts

Finally, let's talk about the cornerstone of your entire financial setup: your escrow accounts. These accounts hold your clients’ money—down payments, closing costs, loan funds. This money is never yours, and it must be handled with extreme care.

Setting up a compliant escrow account involves a few key steps:

- Choosing the Right Bank: You need a financial institution that truly understands the strict rules around escrow or IOLTA (Interest on Lawyers' Trust Accounts). Not every bank does.

- Keeping Meticulous Records: You must maintain separate, detailed records for every single transaction. Commingling funds—mixing money between different clients or with your own operating cash—is a cardinal sin.

- Following Reconciliation Rules: Most states mandate a monthly three-way reconciliation. This process proves that your escrow account balances perfectly match your transaction ledgers and bank statements.

Proper escrow management is the ultimate litmus test for a title company's trustworthiness. Honestly, given how complex it is, this is one area where you’ll thank yourself for investing in modern software. Platforms like TitleTrackr integrate your accounting and file management, making it so much easier to keep compliant, audit-ready records from your very first closing.

This kind of systematic approach doesn't just prevent costly mistakes; it builds a reputation for reliability that will attract the best real estate partners. In an industry where competition is growing, that foundational stability is everything. In fact, the U.S. title insurance market has seen steady growth at a rate of about 3.0% annually, with over 1,000 businesses in the mix. You can learn more about the title insurance market's growth and competitive landscape.

Building a Tech-Driven Operational Workflow

Once you've navigated the legal maze and have your financial house in order, it's time to build the engine that will power your title company. This means defining your operational workflow—the repeatable, ironclad process your team will execute for every single transaction. In this business, one missed detail can derail a closing, so a sloppy workflow isn't just inefficient; it's a massive liability.

Your goal is to create a system that's predictable, transparent, and built for speed. The huge advantage you have as a new company is the ability to build this system around modern technology from the ground up. You get to skip the clunky, paper-drenched processes that bog down so many established competitors. Getting this right is a make-or-break step in launching a title company that can actually scale.

Mapping the Core Closing Process

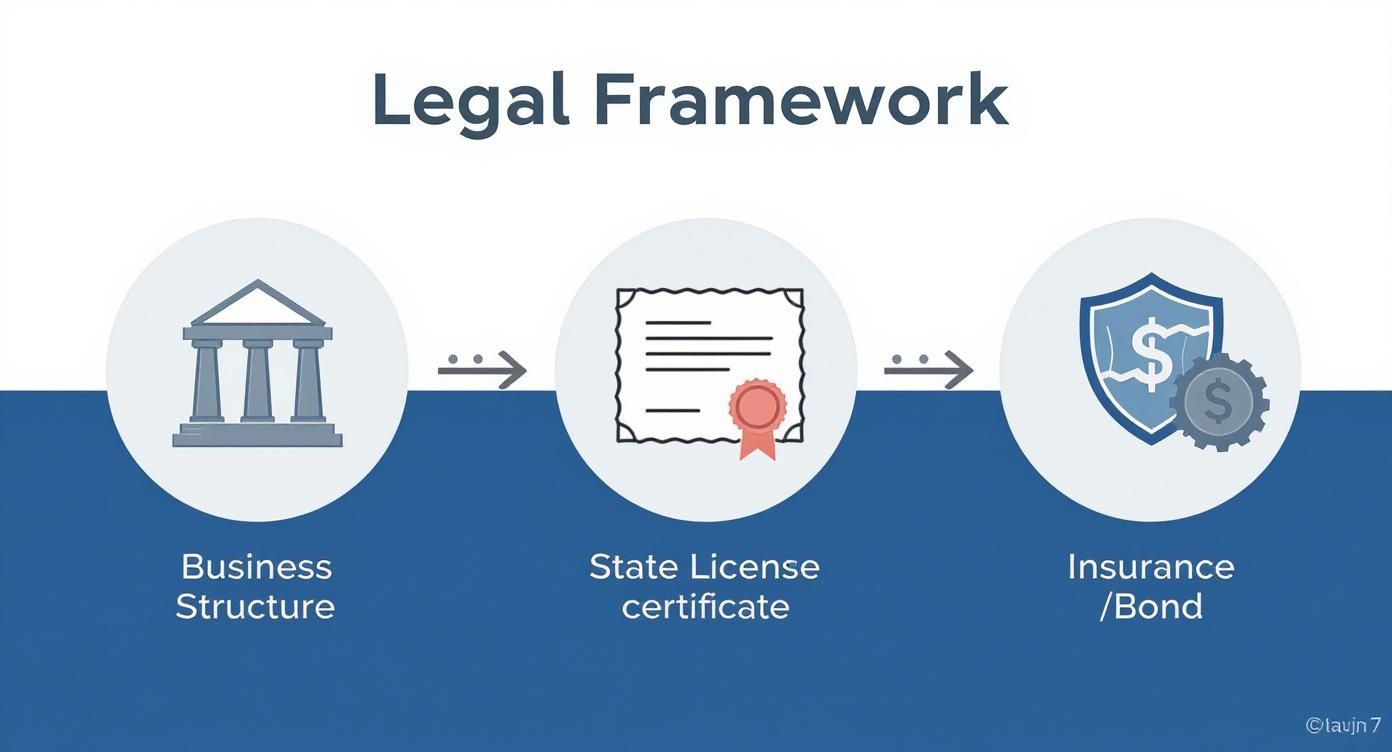

Before you can optimize anything, you need a crystal-clear map of a file's journey from open to close. While every transaction has its quirks, the core process follows a well-worn path.

The infographic below outlines the foundational legal and structural steps you have to complete before you can even think about processing your first order.

Think of these initial steps—forming your business, getting licensed, and securing insurance—as the non-negotiable prerequisites. They're the foundation upon which your daily operations are built.

With those pieces in place, your day-to-day workflow will generally look like this:

- Order Intake: It all starts here. A real estate agent or lender sends over the contract, and you officially open the file in your system.

- Title Search & Examination: Your team dives into the public records, hunting for any liens, judgments, or other clouds on the property's title.

- Curing Title Defects: If you find issues, this is where the real work begins. You'll work to resolve them, which could mean anything from getting a lien released to correcting errors in old documents.

- Closing Preparation: Once the title is clear, your team prepares the settlement statement (like the ALTA Settlement Statement or Closing Disclosure) and coordinates with everyone to schedule the closing.

- The Closing Event: This is the main event. Documents get signed, funds are wired from your escrow account, and the keys (and ownership) officially change hands.

- Post-Closing: The job isn't done yet. This critical final phase involves recording the new deed and mortgage, issuing the title insurance policies, and securely archiving all the transaction documents for compliance.

Each of these stages contains dozens of smaller tasks. A modern, tech-driven workflow is designed to automate as many of them as possible, which dramatically cuts down on human error and frees up your team to handle the truly complex issues.

Selecting Your Technology Stack

Choosing your software is easily one of the most critical decisions you'll make. Your "tech stack" is the collection of tools that will run your entire operation. A patched-together system where different programs don't talk to each other is a recipe for manual data entry, mistakes, and chaos. A unified system, on the other hand, is the key to efficiency.

A modern title company runs on integrated software, not a messy collection of spreadsheets and email chains. Your technology needs to be the central nervous system of your business, connecting every part of the transaction and acting as the single source of truth for your team and your clients.

Here are the absolute essentials you'll need:

- Title Production Software (TPS): This is the heart of your operation. It manages your files, automates document generation, handles your accounting, and keeps you compliant.

- Secure Closing Platform: In today's market, tools for digital closings, including remote online notarization (RON), are no longer a luxury—they're expected. They offer incredible convenience for clients and can significantly speed up the final steps.

- Accounting and Escrow Management: This has to integrate seamlessly with your TPS to ensure flawless, auditable records for your trust accounts. There is zero room for error here.

The real challenge is making all these pieces work together flawlessly. This is precisely why all-in-one platforms are so valuable. A system like TitleTrackr centralizes all of these functions, which eliminates the risky and mind-numbing task of re-entering the same data across multiple programs. When your title production, document management, and client communication all live in one place, your workflow becomes exponentially simpler and more secure.

By investing in a robust, integrated workflow from day one, you build a foundation that's ready for growth. You can handle a higher volume of transactions without having to hire more people, which protects your profit margins and allows your small-but-mighty team to compete with much larger firms.

See how a smarter workflow can completely transform your operations. You can explore a free trial of TitleTrackr and see the difference for yourself.

Assembling Your Expert Closing Team

Your technology and workflows are the engine, but your people are the ones steering the ship. You can have the best systems in the world, but without the right crew in the right seats, you're dead in the water. The success of your new title agency will come down to the expertise, precision, and client-facing skills of the professionals you bring on board.

When you start building your team, you’re not just filling roles. You’re setting the entire tone for your company's culture and reputation from day one. Every single hire is a critical piece of the puzzle, directly shaping your ability to deliver flawless closings and build the kind of trust that keeps real estate agents and lenders coming back.

The Essential Roles on Your Day-One Roster

You don't need a huge staff to get started, but you absolutely need a core group of specialists who can manage the entire transaction lifecycle. You’re looking for people who are not just technically good at their jobs, but who also thrive in a fast-paced, high-stakes environment where a single misplaced decimal can throw everything into chaos.

To get off the ground, your hiring should be laser-focused on these three key roles:

- Licensed Title Agent / Escrow Officer: This person is the cornerstone of your entire operation. They oversee the closing process from start to finish, handle all the legal and regulatory compliance, and are usually the final say on clearing title and disbursing funds. They absolutely must be licensed in your state and have deep industry experience.

- Title Processor: Think of the processor as the operator in the engine room. They’re the ones gathering all the necessary documents, coordinating with lenders, agents, buyers, and sellers, clearing up title issues, and getting the file ready for the closing table. This role demands insane organizational skills and a proactive communication style.

- Title Searcher / Abstractor: This is your investigator. This specialist digs into public records to build the title abstract, which lays out the property's entire history. While some agencies outsource this work, having a trusted in-house expert or a go-to partner is a game-changer for quality control and speed. You can learn more about the vital work of title abstractors and how technology is shaping their role.

Identifying Top-Tier Talent

When you're writing job descriptions and sitting down for interviews, you have to look beyond the resume. The title business requires a very specific mix of hard and soft skills. Technical know-how is the baseline, but the right personality traits are what separate a decent employee from a great one.

Here’s a breakdown of what you should be looking for:

| Role | Key Responsibilities | Must-Have Traits |

|---|---|---|

| Title Agent | Oversee closings, manage escrow, ensure compliance, build client relationships. | Detail-obsessed, decisive under pressure, strong leadership, impeccable ethics. |

| Processor | Manage files, clear title defects, communicate with stakeholders, prepare documents. | Hyper-organized, excellent communicator, problem-solver, thrives on checklists. |

| Abstractor | Conduct title searches, analyze public records, identify liens and encumbrances. | Analytical mindset, investigative, highly methodical, patient and thorough. |

Your first hires set the standard for your entire company culture. Prioritize candidates who are not just skilled but also share your commitment to accuracy, client service, and embracing technology to work smarter, not harder.

Building a Culture of Precision and Service

Once you have your core team, the focus immediately shifts to creating an environment where they can do their best work. A competitive salary is table stakes, but a strong company culture is what keeps top talent around and becomes your biggest competitive advantage.

You need to build a culture that actively rewards:

- Meticulous Accuracy: In this business, "close enough" is a recipe for disaster.

- Proactive Communication: Keep everyone in the loop before they have to call and ask for an update.

- Collaborative Problem-Solving: Encourage your team to put their heads together to crack complex title issues quickly.

By building a team of true experts and giving them efficient, tech-forward workflows, you create a service experience that nobody else can match. This is how a brand-new agency builds a stellar reputation and turns first-time clients into long-term referral partners.

Winning Clients and Marketing Your New Agency

You’ve done the hard work. Your legal framework is solid, your operational workflow is humming, and you have a stellar team ready to go. Now for the most critical part of launching a title company that actually succeeds: getting business in the door.

No matter how smooth your back-end systems are, they don't mean a thing without a steady stream of closing orders. This is where the real hustle begins. You're not just selling a service; you're selling trust in an industry that runs on decades-old relationships.

What's Your Compelling Value Proposition?

Before you spend a dime on marketing, you have to nail the answer to one simple question: "Why should a busy real estate agent or lender ditch the company they've used for ten years and give my brand-new agency a shot?"

Your answer is your value proposition, and it needs to be razor-sharp. Generic promises like "we have great service" are noise. They won’t get you anywhere. You need to pinpoint what makes you genuinely different.

Maybe your edge is sheer speed. You've built a tech-forward operation that guarantees a title commitment in 24-48 hours while the competition takes a week. Or perhaps it’s total transparency—a modern client portal where agents and their clients can see real-time status updates 24/7, no phone calls needed.

Your value proposition isn't a fluffy marketing slogan. It's the core promise you make to every client. Zero in on tangible benefits like faster closings, fewer mistakes, and proactive communication. That's how you break through and convince established pros to take a chance on you.

Whatever your "it" factor is, it has to be the central theme of every single marketing effort you make.

Building Your Network of Referral Partners

The lifeblood of any title agency is its referral network. Period. Your primary targets are the local professionals who control the flow of transactions.

- Real Estate Agents: They are on the front lines with buyers and sellers. Earning their trust is your absolute number one priority.

- Mortgage Lenders and Brokers: They need a title partner who closes loans fast and clean. Any delay on your end puts their funding timeline at risk.

- Real Estate Attorneys: In many markets, attorneys are central to the deal and their recommendation for a title company carries serious weight.

Don't be the person who just shows up with donuts and a stack of business cards. That's not a strategy. You need a real plan. Get active in your local real estate association meetings. Offer to teach a continuing education class on common title defects. Host a "lunch and learn" for a top-producing brokerage. Provide real value first.

Your Digital and Traditional Marketing Mix

The best results come from a balanced approach. You need a polished digital presence to build credibility and a relentless traditional networking game to build those crucial personal connections.

Your online foundation is a clean, professional website. It must clearly state your value proposition, introduce your team, and make it ridiculously easy for someone to place an order or request a quote.

Beyond the site, pour your energy into Local SEO. You want to be the first name that pops up when an agent in your city searches for "title company near me." This means you have to:

- Create and meticulously fill out your Google Business Profile.

- Start gathering positive online reviews from your first few happy clients.

- Make sure your website content is packed with local keywords and service area information.

On the traditional side, focus your energy. Identify the top 20% of agents and lenders in your market who are doing 80% of the business. These are the handful of relationships that will make or break your first year.

Turn Your Tech into a Marketing Weapon

Here’s where a new agency has a massive, built-in advantage. Your technology isn't just for making your team efficient; it's one of your most powerful marketing tools. You can offer a client experience that older, less agile competitors can't dream of matching.

When you use a modern platform, you can offer features that directly solve the headaches of your referral partners. For instance, a secure client portal that provides real-time updates and document access isn't just a nice-to-have, it's a huge selling point.

Imagine walking into a brokerage and telling an agent: "Work with us, and you'll never have to call my office for a status update again. You and your client can log in anytime, day or night, and see exactly where the file stands."

That's not just a convenience. You're giving them back their time and reducing their stress. By showing how your tech creates a smoother, more transparent closing, you turn an operational choice into a compelling reason to choose you. This is what builds real loyalty and generates the powerful word-of-mouth referrals that will fuel your agency for years to come.

Frequently Asked Questions About Starting a Title Company

Jumping into the world of title can feel like drinking from a firehose. You’ve got questions, and rightly so. Let’s tackle some of the most common ones I hear from entrepreneurs looking to make their mark.

How Much Capital Do I Need to Start a Title Company?

There’s no single magic number, as startup costs swing pretty wildly from state to state. But a realistic budget usually lands somewhere between $50,000 and $250,000.

That range covers the non-negotiables: state licensing fees, surety bonds, and a solid Errors & Omissions insurance policy. You’ll also need to factor in the practical stuff like office space, hiring your first key team members, and investing in your core technology, like title production software. The best way to nail down a precise number is to build a detailed business plan tailored to your specific market.

Can I Run a Title Company Without Being a Licensed Agent Myself?

In most states, the answer is yes, but with a big asterisk. You absolutely can own and manage the company, but you are required to have a designated, licensed title agent on your team. This person is legally responsible for overseeing all title and escrow activities.

Think of them as your compliance backstop. While you steer the ship, you need a qualified professional to ensure every transaction is handled by the book. Rules vary, so make sure you double-check the specific regulations in your state.

What Is the Biggest Challenge for a New Title Company?

Without a doubt, it’s breaking into established networks. Your biggest hurdle will be building relationships and winning a steady stream of business from real estate agents and lenders who have been working with the same title companies for years.

This is where you have to get scrappy and smart. New companies can’t compete on legacy; they have to compete on service. That means faster closing times, crystal-clear communication, and a smoother experience for everyone involved. This is often where modern technology gives you a huge advantage over older, more entrenched competitors.

The key is to turn your agility into a weapon. Focus on delivering a client experience that is so transparent and efficient that referral partners have a compelling reason to switch from their long-time providers.

How Do Title Companies Make Money?

It really boils down to two main revenue streams: title insurance premiums and closing or settlement fees.

When a property is sold or refinanced, your company gets a cut of the insurance premium. On top of that, you charge fees for all the work that goes into the closing itself—things like title searches, document preparation, and conducting the final settlement.

If you want to dig deeper into the nuts and bolts, you can explore our full list of frequently asked questions for more industry insights.

Ready to build your title company on a foundation of speed and accuracy? TitleTrackr provides the AI-driven tools to automate your workflows, reduce errors, and deliver an exceptional client experience from day one. See how our platform can give your new agency a competitive edge. Request a demo at https://titletrackr.com.

Leave a comment