Foreclosing on a lien is the ultimate legal tool for turning an unpaid debt into a tangible recovery by forcing the sale of a property. It’s a serious step, but when you've exhausted all other options, it’s often the only way to secure the payment you're owed. This guide provides the insights your business needs to navigate this complex process, minimizing risk and maximizing your chances of a successful outcome.

Understanding the Lien Foreclosure Process

Once you've confirmed your legal right to foreclose, a very specific legal process kicks into gear. This isn't something you can just wing; it involves a strict sequence of notices, court filings, and non-negotiable deadlines that demand precision.

The first thing to nail down is the type of lien you hold, because that dictates your entire strategy.

- Mortgage Liens: These are the most common, securing home loans. The rules are baked into state law and can be incredibly specific.

- Mechanic’s Liens: This is a contractor's best friend. If you’ve done work or supplied materials and haven't been paid, this lien protects your right to compensation.

- Judgment Liens: These come from a court order. If you win a lawsuit and the defendant doesn't pay up, a judgment lien attaches to their property.

Let's look at a real-world example. A Houston contractor built a custom porch for a homeowner, but the final $12,000 payment never came. She correctly filed a mechanic's lien within the six-month window, which preserved her rights. When the homeowner still refused to pay, she initiated foreclosure. The property was sold, and she recovered her $12,000 plus her attorney's fees.

Had she missed that six-month filing deadline, her claim would have vanished. Poof. Gone.

Lien Priority Is Everything

Here's a critical concept you can't ignore: lien priority. This determines the pecking order of who gets paid when the property is sold at auction. If you're a junior lienholder, you could end up with nothing if senior liens (like the primary mortgage) eat up all the proceeds from the sale.

You absolutely have to know your place in line before you spend a dime on filing a foreclosure action.

This isn't just a theoretical problem. Recent data shows foreclosure filings have climbed by 5.8%, impacting 187,659 properties. That's roughly 1 in every 758 housing units in the country. If you want to dive deeper into the numbers, you can check out these foreclosure statistics from Kaplan Collection Agency.

The rising trend underscores just how important it is to get every step of the process right.

The Key Stages of a Lien Foreclosure Action

To make sense of the journey, it helps to break down the core phases of a foreclosure lawsuit. While the specifics can change from state to state, the general roadmap looks like this.

| Stage | Primary Goal | Key Action Required |

|---|---|---|

| Initial Filing | Officially notify the property owner and the court of the intent to foreclose. | File a formal complaint (lis pendens) or notice of foreclosure with the court. |

| Service of Process | Legally inform all involved parties that the foreclosure action has begun. | Properly serve the summons and complaint to the property owner and other lienholders. |

| Public Auction | Sell the property to the highest bidder to satisfy the debt. | Publish the notice of sale and conduct the auction according to state law. |

| Post-Sale Resolution | Distribute the sale proceeds to the lienholders according to priority. | Allocate funds to pay off debts and handle any surplus or deficiency. |

Each of these stages is a potential minefield. A single misstep in documentation or a missed deadline can send you right back to the start, costing you time and money.

Your Strategic Checklist Before You File

Before you even think about heading to the courthouse, there are a few things you must do to set yourself up for success.

- Run a comprehensive title search. You need to know every single claim against the property. No surprises.

- Calculate the full debt. This isn't just the principal. Add up all the accrued interest, late fees, and legal costs.

- Double-check your notice requirements. Every state has its own rules for how and when you must serve notices. Follow them to the letter.

“A precise notice and a well-timed filing can make or break your foreclosure action. Get it wrong, and you could lose your right to collect entirely.”

This is where a tool like TitleTrackr becomes a game-changer. It automates the title search process and helps you track those all-important deadlines, reducing the risk of a fatal human error and giving your business a competitive edge.

Getting Legal Notices and Deadlines Right

Let me be blunt: if you mess up serving the notice, your case is likely dead on arrival. Courts are absolute sticklers for this.

There are a few standard methods, and you need to use the one required by your jurisdiction:

- Certified Mail: This provides a paper trail and proof of delivery.

- Personal Service: A process server physically hands the documents to the property owner.

- Publication: If you can't find the owner, you may be allowed to publish the notice in a newspaper.

Deadlines are just as unforgiving. Every state and lien type has its own clock for filing the lien, starting the foreclosure, and responding to court actions. Miss one, and your claim is toast.

With these fundamentals down, you're ready to move into the pre-foreclosure stage.

Your Pre-Foreclosure Action Plan

Before you even think about filing a foreclosure lawsuit, you need to lay some solid groundwork. This isn't just about ticking boxes; it's about protecting your claim and making sure there are no nasty surprises waiting for you down the road.

The goal here is simple: uncover any hidden risks and get a crystal-clear picture of where your lien stands in the pecking order.

Conduct a Thorough Title Search

First things first, you need a detailed title search. This isn't optional. It’s the only way to uncover every single existing lien on the property, which is absolutely critical for understanding where you fall in line for repayment.

A proper search will:

- Identify any senior mortgages that get paid before you.

- Spot other claims, like mechanic’s or materialman’s liens, that could affect your standing.

- Confirm there are no undisclosed judgment liens lurking in the background.

Missing even one of these can mean your lien gets pushed to the back of the line, or worse, wiped out completely.

“I’ve seen it happen time and again. Small oversights in a title search can cost a business thousands in lost priority,” says Jane Smith, an industry veteran with over two decades of experience.

Don't cut corners. Always review the full title plant records and double-check county clerk archives to catch any old filings that might still be active. I once saw a supplier in Texas save themselves $15,000 simply because they found an old tax lien before they filed. That's the kind of discovery that makes all the difference.

Calculate Your Total Debt Accurately

Next, you have to crunch the numbers. Is foreclosure even worth the cost and effort? It’s a serious question.

Remember, lenders often roll in interest, late fees, and all sorts of attorney charges that can quickly inflate the total debt. You need a clear-eyed view of your real exposure.

Get your calculator out and tally up:

- The principal and any delinquent interest.

- All late fees allowed under your contract or by state law.

- An honest estimate of legal expenses for filings and notices.

- A projection for court costs, because delays and motion hearings are common.

This isn't just an academic exercise. With U.S. mortgages in active foreclosure recently hitting 0.38%—a jump of 10.47% year over year—you’re facing more competition at auction. Knowing your exact numbers helps you strategize.

Draft and Serve the Notice of Intent

Your Notice of Intent to Foreclose has to be rock-solid, both in its language and how you deliver it. Sloppiness here can get your case thrown out.

I always recommend sending it via certified mail with a return receipt, but personal service is even better if you can manage it. It’s hard to argue with a signed affidavit of service.

Make sure your notice is precise and includes:

- A clear, itemized list of all the debt components.

- The exact cure period the owner has and the consequences of not paying.

- A citation of the specific legal statute that authorizes the foreclosure.

A contractor in Georgia learned this the hard way when his vaguely worded notice was flat-out rejected by the court, setting his case back months.

Foreclosure attorney Mark Rivera notes, “A properly drafted and served notice can reduce an owner’s potential defenses by as much as 40%. It shows you’re serious and have followed the law to the letter.”

You’ll want to serve this notice at least 30 days before you plan to file, but always check your state’s specific requirements because they can vary.

Final Review and Practical Tips

Before you march down to the courthouse, do one last sanity check. Double-check every single deadline and service method against your local rules of procedure. Missing a service window can derail the entire process.

I find it helpful to cross-check all my dates in a spreadsheet or calendar tool. It’s a simple step that prevents massive headaches.

Here’s a final checklist:

- Verify your title search findings against the very latest public records.

- Confirm your debt figures one last time with official lender statements.

- Ensure the language in your notice perfectly matches any statutory templates.

For title professionals looking to improve accuracy, check out how top abstractors are using tools like TitleTrackr to speed up their workflow.

One last practical tip: I always pair my digital calendar alerts with a physical, hard-copy reminder. It might seem old-school, but it has saved me from slipping up more than once.

Solid preparation like this is what minimizes objections and gives you leverage once the lawsuit begins. With this pre-foreclosure plan handled, you’re ready to file your suit with confidence.

Filing and Managing the Foreclosure Lawsuit

So, you've decided to move forward and foreclose on your lien. This is where things get serious, and you step into the legal arena. Let’s walk through what actually happens when you file that foreclosure lawsuit.

The whole process kicks off with filing the lawsuit itself. One of the very first things you'll do is file a public notice called a lis pendens. Think of it as a giant, legally binding "heads up" to anyone looking at the property—potential buyers, lenders, you name it. It tells the world that there's an active claim that could affect the property's title.

Filing this notice right away is non-negotiable. It essentially freezes the property's title status, preventing the owner from selling or refinancing it out from under you while your lawsuit is pending.

Getting the Lawsuit Started

Once the lis pendens is on record, it's time to formally serve the complaint on the property owner and any other required parties. This isn’t as simple as just mailing a letter; each state has specific rules about "service," which could mean sending it via certified mail or having a professional process server deliver it in person.

You have to be meticulous here. Missing a service deadline can get your entire case thrown out. I once saw a supplier in Texas lose a perfectly good mechanic's lien because they served the complaint ten days late. A simple mistake cost them everything. Paying close attention to these details can save you months of headaches and potential disaster.

After everyone has been properly served, you'll need to decide which foreclosure path to take. Your options are usually a judicial or non-judicial foreclosure, and they come with very different timelines, costs, and strategic considerations.

- Judicial foreclosures are the traditional route, overseen by the court system. They offer more structure but can be slow, often taking 6 to 12 months to complete.

- Non-judicial foreclosures are faster, relying on a "power of sale" clause in the loan documents. When they're allowed by state law, you can sometimes wrap things up in as little as 90 days.

You'll need to weigh your state's laws, the complexity of your case, and your budget before making a call.

Filing the Paperwork

When you draft your complaint, be thorough. You need to lay out all the facts clearly, citing the relevant laws that support your claim. Make sure you include the property's legal description, the exact debt amount, and details about your lien's priority.

You'll also need to attach the lis pendens and proof that you properly served everyone. Once it's all assembled, you'll submit the package to the court clerk and pay the filing fees, which typically run between $200 and $500. A clean, comprehensive initial filing can head off a lot of potential challenges down the road.

“Precision at filing cuts off most procedural defenses,” notes foreclosure attorney Kara Hill.

Here’s a quick breakdown to help you compare the two main paths:

| Path | Timeline | Cost Range | Court Oversight |

|---|---|---|---|

| Judicial | 6–12 months | $200–$500 | Yes |

| Non-Judicial | 3–6 months | $100–$300 | No |

Bracing for Court Hearings and Owner Defenses

After you file, the property owner gets a chance to respond. And often, they will. They might file motions challenging the validity of your lien, claiming you didn't provide proper notice, or arguing the debt amount is wrong.

This is a critical phase. You need to be prepared to counter these defenses with solid evidence. This is where a tool like TitleTrackr becomes invaluable, as its deadline tracking ensures you never miss a window to file an opposition.

When you get to the hearing, you'll present your case. This means showing the judge clear documentation of the debt and the lien. Sometimes, you might even need affidavits from witnesses. Courts are sticklers for procedure, and they will scrutinize every step you've taken. One small misstep can derail your entire claim. The accuracy and effort you put in here will directly impact how quickly you can move toward a sale.

The Final Stretch: Moving Toward Auction

Once you get a judgment from the court (or file a notice of default in a non-judicial state), you can finally start planning the auction. Each state has different rules for publicizing the sale, like placing ads in local newspapers or posting notices online.

You'll also prepare your "credit bid," which is your opening bid at the auction, usually for the amount of the debt you're owed. If the property sells for more than what you're owed, any surplus funds go to junior lienholders or back to the property owner. It’s crucial to track auction dates carefully to avoid the cost and hassle of rescheduling.

Don't Let Deadlines Derail You

Every single stage of a foreclosure is governed by strict, unforgiving deadlines. Missing just one can be catastrophic for your case. Knowing these dates isn't just good practice—it's essential for keeping your foreclosure on track.

The easiest way to manage this is to use a calendar or specialized software to map out every deadline from the start. I recommend setting reminders for 15, 7, and 1 day before each key date. This simple habit turns a stressful, reactive process into one you can manage calmly and proactively.

Better yet, a platform like TitleTrackr can sync with your calendar and automate these alerts. It gives you a single dashboard to see all your service, filing, and auction windows, dramatically reducing the risk of a costly mistake.

Request a Demo with TitleTrackr

TitleTrackr helps you automate title search tasks, track service deadlines, and manage filing documents. Users report up to 90% efficiency gains when closing foreclosures. See how TitleTrackr fits into your foreclosure workflow by requesting a personalized demo today.

Managing the Foreclosure Sale and Beyond

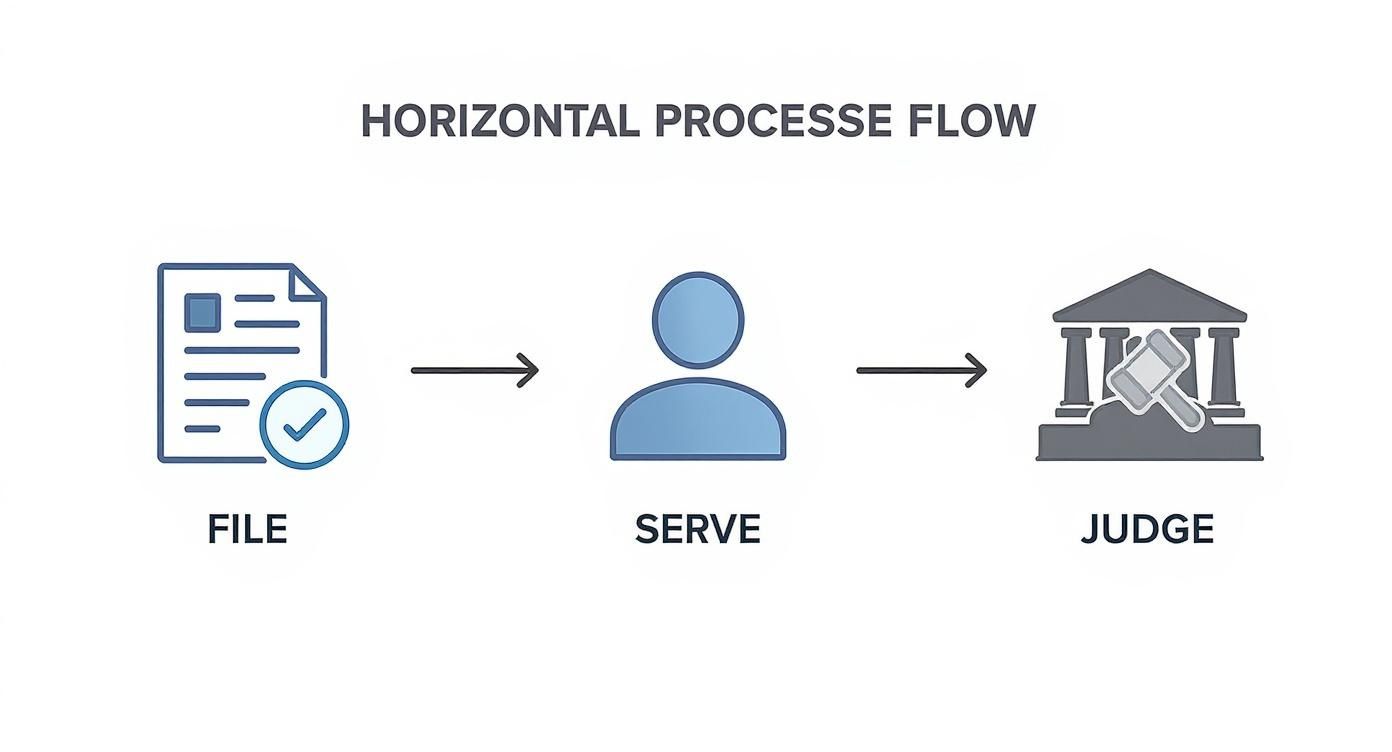

Winning a judgment in court is a huge step, but don't pop the champagne just yet. The finish line is a bit further down the road. Now you have to navigate the actual foreclosure sale and deal with whatever happens next. This is where precision becomes critical—one wrong move and you could jeopardize the entire process.

First up is scheduling and advertising the public auction. I can't stress this enough: every state has its own very specific rules for this. Often, you're required to publish the sale notice in a local newspaper for a set number of weeks. If you mess this part up, the sale can be invalidated, forcing you to start all over again.

This visual gives you a good idea of the legal milestones you've already passed to get to this point.

As you can see, it's a linear path from filing the suit to getting that court judgment in your hands. Each step is a necessary building block for the next.

Preparing Your Bid for the Auction

As the one who initiated the foreclosure, you don't just show up to the auction and hope for the best. You'll prepare what's called a "credit bid." Think of it as using your judgment as currency. It lets you bid up to the full amount you're owed—principal, interest, and legal fees—without bringing a single dollar in cash.

Let's say your total judgment is $75,000. You can bid right up to that amount. If no one bids higher, you become the new owner of the property. It's a strategic play to protect your financial stake and make sure the property doesn't get sold for pennies on the dollar.

Your credit bid is the most important tool you have at the auction. It effectively sets the minimum price, forcing any other interested parties to outbid your claim.

But what if someone does outbid you? That's good news, too. The proceeds from the sale go directly to you first to satisfy your lien. Any extra cash, known as surplus funds, then goes to any junior lienholders based on their priority. If there's still money left over after all debts are paid, it goes back to the former property owner.

When You Become the Property Owner

So, what happens if your credit bid wins? Congratulations, you now own a property. This asset is officially called Real Estate Owned (REO), and your role just shifted from creditor to property manager. This comes with a whole new playbook.

Your immediate to-do list for an REO property should look something like this:

- Secure the Asset: First things first, change the locks. You need to protect the property from squatters, vandalism, or any unauthorized access.

- Handle Occupants: If the old owner or tenants are still living there, you can't just kick them out. You have to follow the letter of the law for eviction, which can be a tricky process.

- Prepare for Resale: Get a handle on the property's condition. Figure out what repairs are needed to get it ready to list on the market and sold.

Managing an REO property introduces another layer of deadlines, expenses, and legal duties. This is where organization is non-negotiable. A platform like TitleTrackr becomes incredibly valuable for keeping tabs on REO assets, managing timelines for evictions or sales, and storing all your documents in one place. By automating these tedious tasks, you can handle the final steps of foreclosing on a lien with a lot more control and a lot less headache.

Common Pitfalls and Strategic Alternatives

Jumping into a foreclosure is a serious move, but believe me, it’s not always the smartest one. Before you commit to what can become a long and expensive legal battle, you need to think strategically. I’ve seen too many people dive in headfirst, only to find themselves tripped up by common mistakes that could have been avoided.

One of the biggest blunders is completely misjudging lien priority. If there’s a senior lienholder out there—like the bank that holds the primary mortgage—and they decide to foreclose, your junior lien can get wiped out. Poof. Gone. You could sink thousands into legal fees and walk away with absolutely nothing if the sale doesn't even cover what they're owed.

Procedural Missteps That Invalidate Your Claim

Even if you have first dibs on the property, simple procedural mistakes can kill your entire case. Courts are sticklers for the rules, and one wrong move could get your foreclosure tossed out, forcing you to start all over again—if you’re lucky.

Here are a few of the most common tripwires I see:

- Improper Notice: You can’t just send an email and call it a day. Failing to serve the property owner and other lienholders exactly as state law dictates—using the right delivery method and hitting every deadline—can invalidate your whole claim.

- Violating Owner Rights: This one is a big deal. If the property owner files for bankruptcy, an "automatic stay" goes into effect, halting all collection efforts. Pushing forward anyway is a serious violation that can land you in hot water.

- Incorrect Filings: Submitting documents with botched debt calculations or the wrong legal description of the property is an open invitation for delays and legal challenges.

These aren't just minor technicalities; they're the foundation of your case. A single error can give the property owner the perfect defense to fight back.

Exploring Smarter Alternatives to Foreclosure

There's a reason foreclosure is often the last resort: it’s a beast. It's expensive, it’s slow, and it’s public. Before you file that first document, it’s worth exploring other paths that could get you paid without the courtroom drama.

It's also worth noting that foreclosure isn't happening uniformly across the country. In the third quarter of last year, while 1 in every 1,402 U.S. homes had a foreclosure filing, certain metro areas saw filings spike by nearly 20% compared to the year before. In these hot spots, everyone is feeling the pressure, which often makes negotiation a much more appealing route for everyone involved. You can see a breakdown of the metros with the highest foreclosure rates to get a better sense of regional risk.

So, what are your options?

- Negotiated Settlement: More often than not, the property owner is just as desperate to avoid foreclosure as you are. A frank conversation can sometimes lead to a lump-sum payment or a manageable repayment plan. This is almost always the fastest and cheapest way to resolve the debt.

- Deed in Lieu of Foreclosure: This is another solid option. The owner voluntarily signs the property title over to you to satisfy the debt. You avoid the uncertainty of a public auction and can wrap things up much more quickly and quietly.

Navigating these alternatives requires a crystal-clear understanding of the property's title status and all associated risks. Accuracy here prevents you from inheriting unforeseen problems along with the property.

Whether you're negotiating a settlement or considering a deed in lieu, a meticulous, up-to-date title search is non-negotiable. You have to know exactly what you’re getting into before you make a move. For a deeper dive into common industry challenges and solutions, you might find some useful insights on the TitleTrackr blog.

Foreclosure Alternatives Comparison

Choosing the right path depends entirely on the specifics of your situation—the property's value, the owner's willingness to cooperate, and your own tolerance for risk. To help clarify the decision, here’s a quick comparison of the options.

| Option | Best For… | Key Pro | Key Con |

|---|---|---|---|

| Foreclosure | Non-cooperative owners or situations where you must enforce your rights legally. | Forces a resolution and can recover the property or debt. | Expensive, slow, and procedurally complex. High risk. |

| Negotiated Settlement | Cooperative owners where a faster, cheaper resolution is possible. | Quick, private, and cost-effective. Maintains control. | Relies entirely on the owner's ability and willingness to pay. |

| Deed in Lieu | When the owner is willing to walk away and the property has clear title/equity. | Avoids the public auction and is faster than foreclosure. | You inherit the property and all its associated liabilities. |

Ultimately, your goal isn't just to foreclose—it's to recover your money as efficiently as possible. The right strategy requires solid information and a clear-eyed assessment of all your options. Making a smart call here can save you a world of trouble down the road.

Lien Foreclosure Questions Answered

When you're dealing with a lien foreclosure, questions are bound to come up. The process is a minefield of legal nuances, and the stakes couldn't be higher. Let's cut through the confusion and get straight to the answers for some of the most common issues people face.

How Long Does It Take to Foreclose on a Lien?

There’s no magic number here. The timeline really hinges on your state’s laws and whether you’re facing a judicial or non-judicial foreclosure. A non-judicial foreclosure, since it sidesteps the courts, can sometimes wrap up in just a few months.

But if it's a contested judicial foreclosure, you could be looking at a year—or even longer. It’s not uncommon for things to get bogged down. If the property owner decides to fight back or files for bankruptcy, the whole process can grind to a halt.

What Happens If There Are Other Liens on the Property?

This is where things get tricky, and lien priority is the name of the game. Generally, liens get paid out from the sale proceeds based on when they were recorded. First in time, first in right.

Here's the kicker: if a senior lienholder, like the bank with the primary mortgage, decides to foreclose, their action can wipe out every junior lien below them—including yours. If the sale doesn't bring in enough cash to cover their debt, you could get nothing. This is exactly why a pre-foreclosure title search isn't just a good idea; it's an absolute must.

Can a Property Owner Stop a Lien Foreclosure?

Absolutely. Property owners have a few powerful moves they can make. The most straightforward is simply paying off the debt in full, which is known as exercising their right of redemption.

They can also take you to court and challenge the validity of your lien itself, maybe arguing you didn't follow the proper procedures to the letter. And don't forget bankruptcy. Filing for bankruptcy triggers an "automatic stay," which instantly freezes all collection activities, including your foreclosure. You have to be ready for these potential roadblocks and have a solid strategy in place.

Getting a handle on these common hurdles is essential before you even think about starting a foreclosure. Every situation just reinforces how critical it is to do your homework and understand your state's specific laws inside and out.

For a deeper dive, check out the detailed answers in our lien foreclosure FAQ section, where we cover a much wider range of scenarios.

Juggling lien priority, owner defenses, and all those procedural deadlines is precisely what TitleTrackr was built for. Our platform gives you the clarity you need to move through the foreclosure process with confidence, automating document analysis and tracking key dates so nothing falls through the cracks. See how you can sharpen your workflow by requesting a demo of TitleTrackr today.

Leave a comment