A report on title is the definitive background check for a property. It's the critical document that investigates a property's history to confirm the legal owner and, crucially, uncovers any hidden baggage like outstanding debts or legal claims that could derail a transaction.

In essence, this report validates that the seller has the undisputed right to sell the property, ensuring the buyer doesn't inherit a host of costly, unforeseen problems. For real estate professionals, mastering this document is key to a smooth closing.

Unpacking the Property's Official Story

You wouldn’t advise a client to buy a business without performing rigorous due diligence. A report on title serves the exact same purpose for real estate, offering a clear window into the property's legal and financial past. It’s not just paperwork; it's the foundation of a secure, defensible real estate transaction.

This report is compiled by a title company, abstractor, or attorney who performs a deep dive into public records. The process involves meticulously sifting through decades of deeds, mortgages, court judgments, tax records, and other legal filings tied to the property. The goal is straightforward: build an unbroken timeline of ownership and flag any issue that could prevent a clean transfer of title.

The Purpose of a Title Report

The concept of a title report dates back to the 19th century, evolving to prevent fraud and settle ownership disputes. Today, it’s an indispensable staple in markets like the United States, United Kingdom, and Canada, where robust property registries enable this detailed investigation. You can learn more about how industry reporting standards have evolved to protect all parties.

A properly researched report provides critical peace of mind and operational certainty.

- It Verifies Legal Ownership: The report confirms the seller is the true legal owner with full authority to transfer the title.

- It Identifies Encumbrances: The search highlights any claims against the property, such as liens, easements granting others usage rights, or unresolved mortgages.

- It Ensures a "Clear" Title: Ultimately, the report's purpose is to determine if the title is free of defects that could challenge the new owner's rights in the future.

Without a thorough title investigation, a buyer could unknowingly acquire a property saddled with hidden debt, or worse, face an ownership challenge from an unknown heir years later. This report is the primary defense against such financial and legal nightmares, making it a cornerstone of your professional responsibility.

Why This Report Is Your Most Critical Document

Moving beyond definitions, the report on title is the single most important safeguard in any real estate deal. A "clear" title is the bedrock of property ownership, and this document is the only tool that verifies its integrity. It transforms an abstract legal concept into tangible proof of ownership.

Think of it as an insurance policy against inheriting someone else's problems. Closing a deal without one is a massive risk, leaving the buyer exposed to financial and legal traps that can surface years after the transaction is complete.

Uncovering Costly Hidden Dangers

Real-world examples highlight the risks of overlooking a title defect. Imagine a client discovering an old, unpaid construction lien from the previous owner's remodel—a debt now legally attached to their property. Suddenly, they could be liable for thousands just to prevent foreclosure.

Another classic scenario is an unknown heir emerging with a legitimate claim to the property. This can trigger a long, expensive court battle that throws the entire ownership into question. These aren't just abstract risks; they are costly realities that a proper title investigation is designed to prevent.

The report on title isn’t just a closing formality; it’s an essential risk-management tool. It delivers the clarity needed to proceed with confidence, ensuring the property is free from the ghosts of its past. Slow, inaccurate reporting creates risks for everyone.

The Key to Securing Financing

Beyond buyer protection, this report is the gatekeeper for mortgage financing. Lenders have a significant financial stake and will not fund a purchase if the title is clouded. They rely on the report to confirm their investment is secure from prior claims or liens.

Simply put: no clear title, no loan. The report is the official green light that signals to the lender that the property is a safe asset to back. This makes it a non-negotiable document not just for the buyer's protection, but for the entire financial structure of the deal.

The data confirms this. In approximately 98% of real estate transactions, the title report uncovers at least one issue that must be resolved before closing. More importantly, properties with clear title reports experience up to 70% fewer legal disputes post-sale, proving the report's value in preventing costly litigation. You can learn more about how these reports stabilize financial transactions worldwide.

How to Read a Title Report, Section by Section

A title report can feel dense with legal jargon, property descriptions, and complex schedules. But understanding its structure unlocks critical information about a potential property, empowering you to guide your clients effectively.

Think of the report as the property's official biography, broken into key chapters. Each section reveals a different part of its story, from its precise physical boundaries to any lingering issues. Navigating these sections is the best defense against spotting deal-breakers before they become costly problems.

The Foundational Elements

Every title report begins with the basics, setting the stage for the detailed findings. This section confirms the core facts of the property and the scope of the search.

Right at the start, you'll find:

- Effective Date: The "as of" date for the report. This signifies that the title company has searched public records up to this point in time and no further.

- Property Information: The common street address and often a parcel number assigned by the local tax assessor.

- Scope of Search: An outline of which public records were examined, such as county land records, tax rolls, and civil court filings.

Deciphering the Legal Description

Following the introductory details is the legal description. This is not the street address. It is the precise, legally recognized definition of the property's boundaries, described so a surveyor could map it exactly. It may use "metes and bounds," reference a plat map, or use a "lot and block" system.

This description is critical because it defines the exact piece of land being purchased. Any discrepancy between this description and the physical property is a major red flag that requires immediate attention.

Understanding Schedule A and Schedule B

The core of the report is typically split into Schedule A and Schedule B. Each has a distinct and vital role in explaining the status of the property's title.

Schedule A is the "good news" section—it tells you what you are getting. It confirms the current owner of record, repeats the legal description of the land, and states the proposed policy amount for the title insurance.

Schedule B, conversely, is where the title company lists any issues, or "exceptions," found during its search. These are the items the title insurance policy will not cover. This section demands full attention, as it's where potential problems are detailed. Common exceptions include:

- Tax Liens: Unpaid property taxes that must be settled before closing.

- Easements: Legal rights granted to another party (like a utility company) to use a portion of the property.

- Covenants, Conditions, and Restrictions (CC&Rs): Rules set by a homeowners' association governing property use.

- Judgments: Court-ordered debts against a previous owner that are attached to the property.

Reading and understanding Schedule B is non-negotiable. It reveals the limitations and obligations tied to the property, showing exactly what kind of baggage the new owner might be inheriting.

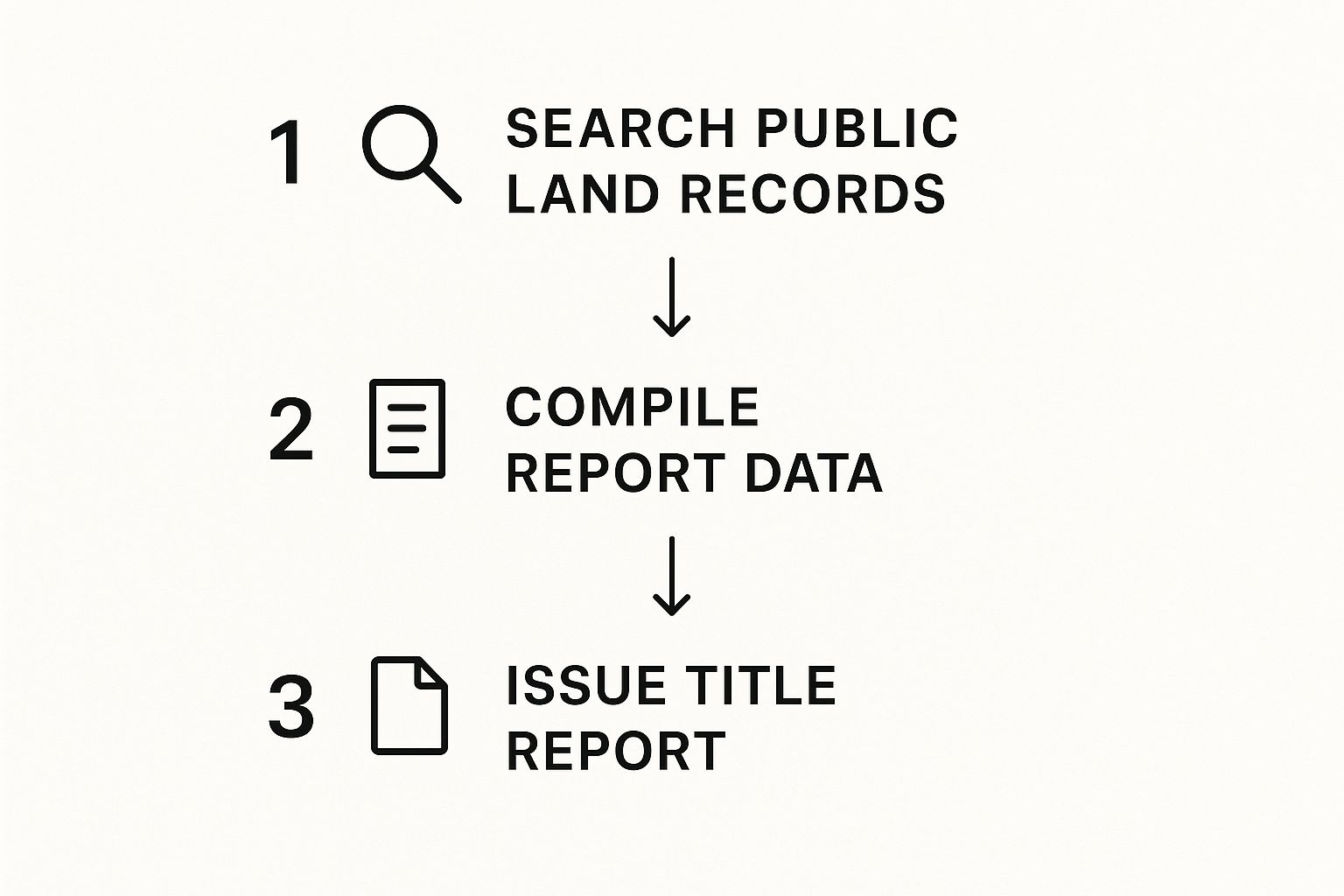

How a Title Search and Report Are Created

The creation of a title report is a meticulous process, combining historical detective work with modern data analysis. The journey starts the moment a report is ordered, kicking off a deep dive into public records archives, a task traditionally handled by skilled title professionals.

These experts—often called abstractors or examiners—comb through county courthouses and digital databases to piece together a property's complete history. They track the chain of title, the chronological sequence of ownership, by examining deeds, mortgages, tax records, court filings, and even divorce decrees. The objective is to build a seamless narrative with no gaps.

This flowchart shows the core steps involved in creating the report.

This visual highlights the progression from raw data collection to a finalized, actionable document that underpins the entire real estate transaction.

From Manual Searches to Modern Automation

Historically, creating a title report was incredibly labor-intensive. It involved physically pulling dusty ledgers or navigating clunky government websites—a process that could take days and was highly susceptible to human error. A single missed document could delay a closing or lead to a defective title.

Fortunately, the industry is rapidly adopting a technology-driven approach. New tools now automate large portions of the title examination process. For instance, AI-powered title searches have cut manual processing time by 20-40%. This tech integration is projected to grow by 15% annually in the title services sector through 2028.

This shift isn't just about speed; it's about precision. By leveraging AI to scan and interpret documents, the risk of overlooking a critical detail is significantly reduced, leading to more reliable and accurate reports.

Platforms like TitleTrackr are at the forefront of this evolution, solving common industry frustrations like unexpected delays and data entry mistakes. By applying AI to analyze records, these tools empower title professionals to work faster and with greater confidence. This sets a new standard for efficiency, helping ensure closings happen on schedule without costly surprises.

For more on how the roles of these professionals are evolving, you can explore our guide on title abstractors.

Navigating Common Title Problems and Their Solutions

Discovering a defect on a title report can be alarming, but it's far more common than you might think. The good news is that most of these issues are fixable. Think of this as a troubleshooting guide for turning potential roadblocks into manageable tasks on the path to a smooth closing.

Instead of viewing a title problem as a deal-killer, see it as a puzzle to be solved. Understanding the issue and mapping out a resolution plan allows you to navigate these hurdles without derailing the transaction.

Unraveling Common Title Defects

A title defect, or "cloud," is any issue that could challenge ownership rights. These can range from a simple typo to a complex claim from a long-lost heir.

Here are a few of the most frequent issues found on title reports:

- Unresolved Liens: These are legal claims on a property for an unpaid debt. A common example is a mechanic's lien filed by a contractor who wasn't paid for a renovation. The property serves as collateral until the debt is settled.

- Errors in Public Records: From misspelled names to incorrect property descriptions, simple human errors can cause significant complications, making it difficult to prove a clear chain of ownership.

- Boundary Disputes: These arise when neighbors disagree on property lines, often due to a misplaced fence, an outdated survey, or conflicting deeds.

Identifying a title defect isn’t the end of the road; it's a critical checkpoint. The purpose of a title search is to catch these problems before closing, protecting your clients from expensive and stressful legal battles down the line.

Charting a Path to Resolution

Once an issue is identified, the path to resolution becomes clearer. Each defect has a standard resolution process, though complexity and timelines vary. For deeper insights into complex scenarios, you can always find resources on our real estate industry blog.

To help you understand what to expect, here is a quick-reference guide.

Resolving Common Title Defects

This table breaks down common title problems, explains their potential impact, and outlines the typical steps required for resolution.

| Common Issue | Potential Impact | Typical Resolution Path |

|---|---|---|

| Unresolved Liens | Halts the sale until the debt is paid, as the lien holder has a legal claim on the property. | The seller must pay the outstanding debt. The lien holder then files a "release of lien" document with the county to clear it. |

| Errors in Public Records | Creates confusion over legal ownership and can delay or even stop a lender from financing the deal. | A corrective deed or another legal instrument is filed to officially amend the public record and fix the mistake. |

| Boundary Disputes | Can lead to lawsuits and negatively affect the property's value and how it can be used. | A new property survey is ordered. Neighbors may need to sign a formal boundary line agreement to resolve the dispute for good. |

| Undisclosed Heirs | An unknown heir from a previous owner could surface with a valid claim to the property, challenging the sale. | The title company works to identify all legal heirs and have them sign quitclaim deeds, which transfers their interest away. |

| Illegal Prior Deeds | A past deed might be invalid due to forgery, a signature from a minor, or another legal flaw. | A "quiet title" lawsuit may be required. This asks a court to make a final judgment on who the rightful owner is, clearing the title. |

While this table covers the basics, every situation is unique. The key is to work closely with your title company or real estate attorney to ensure every cloud is cleared well before the closing table.

Modernize Your Closings with Faster Title Reporting

In any real estate transaction, a clear report on title isn’t just important—it’s absolutely non-negotiable. The problem is that the traditional process is often painfully slow, opaque, and riddled with the potential for human error. These are the kinds of mistakes that can stall a closing, damage your reputation, and frustrate clients.

That friction is no longer necessary. Instead of waiting days for manual record reviews, modern technology offers a better path forward. Imagine delivering accurate, detailed reports in a fraction of the time, eliminating the bottlenecks that have defined this industry for decades.

Embrace a More Efficient Workflow

The difference between outdated and modern methods is stark. The traditional approach is weighed down by manual data entry and document review, creating delays at every turn. This is precisely where AI-driven platforms provide tangible benefits that solve these long-standing headaches.

- Accelerate Turnaround: Slash report generation times from days to mere minutes, keeping your transactions on schedule.

- Enhance Accuracy: Drastically reduce the risk of costly errors with intelligent data extraction that captures every detail.

- Elevate Client Service: Deliver a smoother, more reliable experience for clients who expect modern efficiency.

Stop letting archaic processes dictate your timeline and your clients’ satisfaction. The tools are here today to completely transform how you handle title reporting, giving you a sharp competitive edge.

It’s time to move beyond the limitations of the past. By adopting a streamlined, modern solution, you aren't just improving operational efficiency—you are fundamentally elevating the quality of service you provide.

See for yourself how TitleTrackr is revolutionizing the industry. Request a demo today and discover how our platform can transform your closings.

Frequently Asked Questions About Title Reports

Even with a thorough understanding, a few practical questions often arise. Here, we'll tackle some of the most common queries from buyers, sellers, and real estate professionals.

Think of this section as a final clarification of the real-world details that come up between ordering a report and closing a deal.

How Long Is a Report on Title Valid?

A title report is a snapshot in time, reflecting a property’s public records at the exact moment the search was completed. Because of this, it doesn't have a formal expiration date, but its accuracy diminishes quickly. A new lien or claim can be filed at any moment, changing the title's status.

Most lenders will not accept a report that is more than 30-90 days old. To ensure nothing has changed, title companies perform a final title update right before closing to catch any last-minute issues.

What Is the Difference Between a Title Report and Title Insurance?

This is a critical distinction. An analogy makes it clear: the title report is the diagnosis, and title insurance is the protection plan.

The report is the investigative work. It is the result of a deep dive into public records to identify any existing problems with the title. All known issues are brought to light here.

Title insurance, on the other hand, is the policy that protects the owner (and their lender) from financial loss if a title defect was missed during that search. Any problems found in the report are listed as "exceptions," meaning the insurance policy will not cover those specific, known issues.

For more answers to common questions, head over to our comprehensive TitleTrackr FAQ page.

Ready to stop waiting and start closing? TitleTrackr uses AI to deliver precise, comprehensive title reports in a fraction of the time. Request a demo today and see how you can modernize your workflow.

Leave a comment