When you're calculating a mortgage payoff for a closing, you’re looking for a single, precise number that settles the entire debt. It's the sum of the outstanding principal balance, any accrued daily interest up to the payoff date, and any other lender fees. For title agents and real estate professionals, this final figure is mission-critical to closing the loan account and ensuring a clear title.

Understanding a Mortgage Payoff Calculation

Before diving into the math, it's crucial for industry professionals to understand what a mortgage payoff amount represents. It’s far more than the remaining balance on a monthly statement. Think of it as the final, all-inclusive bill required to terminate the loan and release the lien.

This number is a moving target, changing daily due to per diem interest. For real estate and title pros, explaining this clearly and confidently is non-negotiable. One inaccurate calculation can cause closing delays, frustrate clients, and create financial shortfalls that jeopardize the entire transaction.

The Role of the Amortization Schedule

The key to understanding a mortgage payoff is wrapped up in the loan's amortization schedule. This schedule is the roadmap for the life of the loan, breaking down how every payment gets split between principal and interest.

Early in a mortgage, the lion's share of a payment goes straight to interest. As the loan matures, more of each payment starts chipping away at the principal. This is precisely why the payoff amount isn't just a simple subtraction from what was originally borrowed.

A huge misconception among consumers is that the payoff amount is a fixed number. It's not. It changes daily as interest accrues. A quote you get on a Monday will be different by Friday, which is why nailing down the specific payoff date is absolutely critical for a smooth closing.

For any professional in this business, explaining this concept to clients is a must. It helps them understand why the number they see on their statement isn't the final word. To help you calculate and communicate the numbers behind the payoff, we've broken down the key components you'll find on any official statement.

Key Components of a Mortgage Payoff Statement

This table breaks down the essential elements found in a typical mortgage payoff statement, helping professionals quickly identify and understand each part of the calculation.

| Component | Description | Why It Matters for an Accurate Payoff |

|---|---|---|

| Principal Balance | The remaining amount of the original loan that is still owed. | This is the foundation of the payoff amount. Without this number, you can't even begin the calculation. |

| Accrued Interest | The interest that has accumulated since the last payment was made. | Interest is calculated daily. The payoff must account for every day up to the closing date. |

| Payoff Date | The specific date the funds will be received by the lender. | This date determines how many days of accrued interest to include in the final total. |

| Prepayment Penalties | Fees charged by some lenders if a loan is paid off before a certain time. | These can add thousands to the payoff amount and must be identified early in the process. |

| Recording Fees | Costs associated with officially recording the release of the mortgage lien. | A small but necessary fee to ensure the title is cleared of the old mortgage. |

| Statement Fee | A fee some lenders charge simply for generating the payoff statement. | Another administrative cost that needs to be factored into the final number. |

Getting a handle on these components demystifies the payoff process. It's not just one big number; it's a collection of specific costs that, when added together, represent the total amount needed to satisfy the loan.

How Extra Payments Impact Your Payoff

Making extra payments directly toward the principal can completely change the game. It’s one of the most powerful strategies for building equity faster and saving a fortune in interest.

For example, on a $372,217 mortgage with 25 years left, just adding an extra $500 a month could cut the loan term down to a little over 17 years. The real kicker? That move could save you around $122,306 in interest. That's paying roughly 26% less in total interest over the life of the loan.

This works because every extra dollar applied to the principal shrinks the base on which future interest is calculated—a core concept in any mortgage payoff. If you want to play with the numbers yourself, check out this great mortgage tool from Calculator.net to see how different scenarios could play out.

The Core Variables That Drive Your Calculation

When it comes to a mortgage payoff, precision is everything. For real estate and title pros, a single wrong number can bring a closing to a screeching halt, leaving clients frustrated and transactions in limbo. Getting it right comes down to nailing a few key inputs that form the foundation of the entire calculation.

Think of it this way: the payoff formula is only as good as the data you feed it. At the heart of it all are three crucial pieces of information. Without them, you’re just guessing.

- Current Principal Balance: This isn't the original loan amount. It’s the exact amount owed on the loan right now, and it's the absolute starting point for any payoff quote.

- Exact Interest Rate: Close enough doesn't cut it. You need the specific annual rate to calculate the per diem (daily) interest that accrues until closing.

- Remaining Loan Term: Knowing how many months or years are left on the mortgage is key for verifying amortization schedules and ensuring all the numbers line up.

A classic mistake is grabbing the original loan amount or miscalculating how many payments are left. These slip-ups seem small, but they can throw the final payoff figure off by hundreds or even thousands of dollars.

Fixed vs. Adjustable Rate Nuances

The type of loan you're dealing with completely changes the game. A fixed-rate mortgage is straightforward—the interest rate never changes, so calculating the daily interest is simple.

But an adjustable-rate mortgage (ARM) is a different beast entirely. Here, the rate can change after an initial fixed period, which means you have to be extra careful.

For any ARM, you absolutely must confirm the current interest rate, not the one from the start of the loan. These mortgages, often with initial terms of 5, 7, or 10 years, can have their rates reset, and it’s a critical detail that’s easy to miss with manual checks.

Imagine a borrower with a $300,000 loan at a 4% fixed rate who has 20 years left. Their payoff is relatively easy to project. But if that rate could change next month, the whole calculation gets more complex. As you can explore with various payoff scenarios, the longer the term and higher the rate, the more interest builds up—making every number critical.

Digging up these details by calling lenders or logging into clunky portals is more than just a time-sink; it's a recipe for human error. A misplaced decimal or an old interest rate can torpedo an entire closing.

This is exactly where automation makes a world of difference. A system like TitleTrackr sidesteps these risks by pulling accurate, real-time data directly from the lender. It guarantees every variable is up-to-the-minute, preventing the costly errors that plague manual payoff calculations.

Ready to see how you can solve these challenges? Request a demo and see TitleTrackr in action.

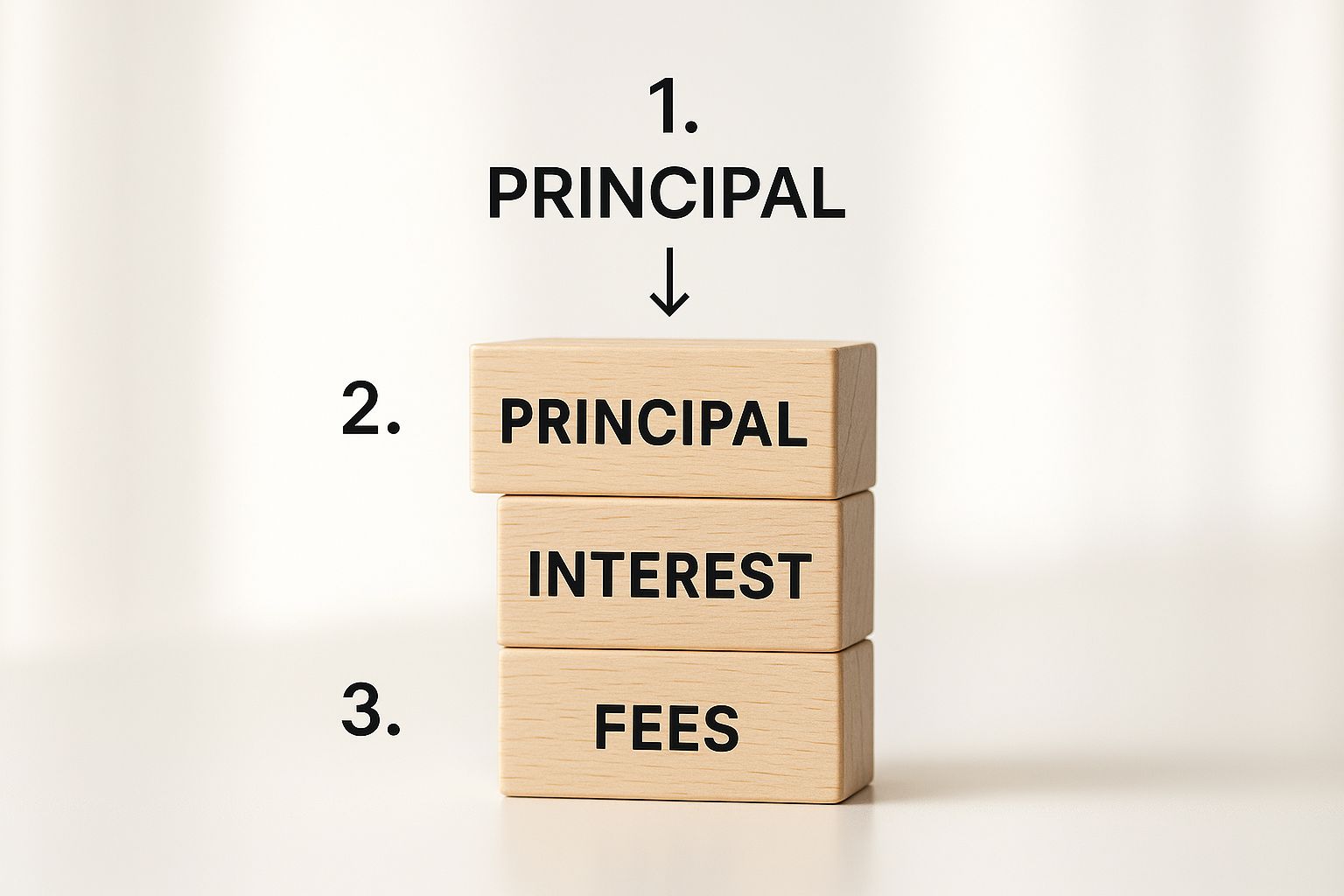

How the Amortization Formula Really Works

To really get a handle on mortgage payoffs, you have to look under the hood at the amortization formula. This is the engine that drives every single payment, dictating exactly how it’s split between what you owe and what the lender earns.

It’s a powerful calculation designed to zero out a loan over a set term with fixed payments. But the real magic is in that principal and interest split.

This infographic breaks down the core components the formula is constantly balancing.

As you can see, the formula is always rebalancing these elements with every single payment you make over the life of the loan.

The Front-Loaded Interest Effect

In the early years of a mortgage, your payments are almost all interest. It’s a hard truth. A huge chunk of your money goes straight to the lender, while just a tiny fraction chips away at your actual loan balance.

For instance, on a $300,000 loan, it’s not uncommon for the first payment to see over 70% of it get eaten up by interest.

Over time, this dynamic completely flips. Toward the end of the loan, those last few payments are almost entirely principal. This gradual shift is the very essence of amortization, and it's why you can't just multiply your payment by the months left to get a payoff amount.

Understanding this front-loaded interest is key when advising clients. It perfectly explains why their principal balance barely seems to budge in the first few years, even when they’re making those big monthly payments on time.

Different Loan Types, Different Formulas

Now, not all loans play by these exact rules, which can make payoff calculations tricky. While most fixed-rate mortgages use standard amortization, other products have their own unique math.

A 5-year balloon loan, for example, calculates your monthly payment as if it were a 30-year loan. But after just five years, the entire remaining balance is due in one massive lump sum. This can mean a final payment of over 90% of what you originally borrowed.

Getting a firm grasp on these different calculation methods is crucial for accurate financial planning. You can learn more about loan payment calculations here.

Hidden Costs That Change Your Payoff Amount

Getting that final payoff quote should be simple, right? You’d think it’s just the remaining principal plus a little interest. Unfortunately, it’s rarely that straightforward.

We’ve all seen it: a payoff quote comes in higher than expected, catching clients completely off guard and threatening to throw a wrench in a smooth closing. Getting ahead of these overlooked costs is the key to managing everyone’s expectations and keeping the transaction on track.

The most common culprit is per diem interest. This is the daily interest that adds up between the borrower's last payment and the exact day the lender gets the payoff funds. It’s a small amount each day, but it’s precisely why the payoff date is so critical. If a closing gets delayed by even one day, another day of interest gets tacked onto the total.

But it's not just the daily interest. A few other fees can creep in and inflate the final number, turning what should be a simple calculation into something much more complex.

Fees and Penalties to Watch For

Any seasoned title professional has a story about a closing getting complicated by last-minute, unexpected charges. These usually pop up as a mix of administrative costs and forgotten contractual obligations that have to be settled before the loan can be officially closed out.

Here are a few of the usual suspects that can sneak into a payoff amount:

- Prepayment Penalties: You don't see these as often anymore, but some loans—especially older ones from the early 2010s or certain non-qualified mortgages—have a clause that slaps the borrower with a fee for paying off the loan too early. This can be a huge cost, often calculated as a percentage of the remaining balance.

- Recording Fees: This is a simple administrative fee charged by the county to officially record the release of the mortgage lien and clear the property's title.

- Statement or Fax Fees: Believe it or not, some lenders will charge a small fee just for the service of preparing and sending the official payoff statement.

- Negative Escrow Balance: This one is common. If property taxes or insurance premiums were recently paid from the escrow account and there wasn't enough cash in it to cover the bill, that shortfall gets added to the payoff total.

Imagine your client is refinancing a loan that has a prepayment penalty equal to six months of interest. On a $250,000 loan with a 6% interest rate, that penalty alone adds a shocking $7,500 to the payoff amount. That's the kind of surprise nobody wants at the closing table.

Trying to anticipate and track down every one of these potential costs manually is not just a huge time-sink; it's also a recipe for errors. This is where an automated system like TitleTrackr makes a world of difference. It can help flag these items quickly by pulling comprehensive, real-time data directly from lenders, ensuring every closing is built on accurate figures right from the start.

Why Manual Calculations Are Holding You Back

If your team is still calculating mortgage payoffs by hand or wrangling with clunky lender portals, you're doing more than just wasting time—you're introducing unnecessary risk into every transaction.

Every manual calculation is a minefield for human error. It could be a simple typo, a misplaced decimal, or a misunderstanding of a complex fee structure. In this business, these "small" mistakes have massive consequences. A single miscalculation can blow up a closing, damage your company's reputation, and leave your team scrambling to cover a financial shortfall.

The Limits of Traditional Methods

Sure, generic online calculators can provide a ballpark figure, but they are no substitute for a verified, official payoff statement from the lender. They almost always miss the critical details that can swing the final number.

These tools are notorious for overlooking key variables like:

- Per diem interest: Most calculators can’t accurately project daily interest charges out to a specific closing date.

- Escrow accounts: They have no idea what the real-time balance of a borrower's escrow account is, so they can't account for shortages or overages.

- Lender-specific fees: Things like recording charges, statement fees, and other administrative costs are almost never baked into their formulas.

Relying on these rough estimates just sets false expectations for your clients. It leads to confusion and frustration at the closing table when the real numbers finally show up.

Relying on manual data entry and delayed information doesn't just slow you down; it opens the door to costly compliance risks. An inaccurate payoff can lead to title defects and post-closing headaches that could have been easily avoided.

This is exactly why top-performing title agents and lenders are leaving these risky, old-school methods behind. The goal isn't just about speed; it's about delivering a level of accuracy and client satisfaction that manual processes simply can't match.

There's a much better way to handle these complex tasks. You can discover it for yourself by checking out a free trial of automated workflow tools designed to eliminate these risks entirely. Modern solutions give you the confidence that every single calculation is precise, every single time.

Ditch the Payoff Panic with TitleTrackr

Let’s be honest: chasing down mortgage payoff figures is a grind. It’s a mess of endless phone calls, tedious manual data entry, and that last-minute knot in your stomach when you worry a number might be off. What if you could eliminate that entire workflow?

That’s exactly what automation tools like TitleTrackr do. Instead of your team chasing data, TitleTrackr integrates directly with lenders to pull real-time, accurate payoff numbers automatically.

This isn’t just a minor improvement; it’s a complete process overhaul. The direct lender connection takes human error out of the equation. Forget about typos or working with outdated interest rates. The system automatically calculates per diem interest right up to the closing date, giving you a crystal-clear, reliable payoff figure in seconds.

How This Changes Your Closings

For title agents and real estate pros, this means closings get faster and more transparent. Period. This kind of accuracy eliminates those awful closing-day surprises that derail transactions and leave clients frustrated. Instead of burning hours tracking down figures, you can focus on giving every client a smooth, professional experience.

The real cost of manual payoffs isn't just the time you lose; it's the trust you risk. An automated system gives you a defensible, accurate number every single time, which builds confidence and protects your reputation with every deal you close.

This precision is especially critical for specialists like title abstractors, whose work depends entirely on getting the data right to deliver clean title reports. When the data retrieval is automated, they can spend their valuable time on what really matters: complex title examinations and analysis.

Ultimately, automation is the answer to the headaches that have plagued the manual payoff process for years. It brings a level of speed and precision that older methods just can't touch, leading to smoother operations and much happier clients. With the average U.S. mortgage balance hitting $252,505 in 2024, the stakes are simply too high to leave room for error.

Ready to see how you can solve these challenges? Request a demo and see TitleTrackr in action.

Common Questions About Mortgage Payoffs

Even when you've run the numbers and think you have it all figured out, mortgage payoffs can still throw you a curveball. It’s one of those areas where small misunderstandings can snowball into big closing day headaches and frustrated clients.

Let's walk through a couple of the questions that come up time and time again. Getting these right isn't just about the math; it's about showing your clients you're on top of every detail.

Why Is My Payoff Amount Higher Than My Principal Balance?

This is probably the most common point of confusion we see. A client looks at their latest mortgage statement, sees the principal balance, and assumes that’s the final number. But the payoff quote always comes in higher. Why?

It all comes down to accrued interest. Lenders calculate interest on a daily basis (this is often called per diem interest). So, the payoff quote has to account for not just the outstanding principal, but also all the interest that has piled up since the last payment was made, right up to the day the funds are received.

How Does an Extra Payment Affect My Mortgage Payoff?

Making an extra payment is a smart move, especially if you tell your lender to apply it as a "principal-only" payment. Doing this directly chips away at your outstanding principal balance.

This is powerful because it immediately lowers the base amount that your future interest is calculated on. When it's time to generate a payoff quote, the starting point is that new, lower principal, which naturally leads to a smaller final payoff amount. It's a direct way to save money and get to the finish line faster.

Payoff quotes are incredibly time-sensitive. Most are only valid for 10-30 days. It's crucial to get an updated quote as close to the closing date as you can. If a closing gets delayed, you absolutely have to request a new one, because that daily per diem interest keeps adding up, changing the total amount owed.

For a deeper dive into these and other closing-related topics, check out our frequently asked questions about title and closing processes. Understanding these details helps ensure there are no last-minute surprises at the closing table.

Stop letting manual errors and slow lender responses dictate your closing schedule. With TitleTrackr, you can get instant, accurate payoff data directly from the source, eliminating costly mistakes and ensuring every transaction closes smoothly. Request a demo today!

Leave a comment